The PE Donut Hole

There is a recurring dynamic in nearly every PE career where the math on paper looks fantastic. Net worth is growing. Carry is vesting. And yet financial decisions feel heavier than they did five years earlier, even though the balance sheet says they shouldn’t.

I know how it sounds. Champagne problems. The world’s smallest violin. Most of the clients have even said it about themselves at one point or another. Even so, the dynamic is real.

I refer to this period as the donut hole.

The most important thing to understand about it is that it is not a single phase. It is a pattern that returns at different stages of wealth, scaled to wherever you are at the time. The dollar amounts change. The proportions can feel the same.

Picture your financial position as a donut. Real value is building around the perimeter in the form of illiquid carry, marked co-investments, retirement plans, 529s, and long-term public equity exposure you’d prefer not to touch. But in the center, where you need accessible cash to live your life, there is a gap.

If everything happens in the right order, the gap closes itself. The first meaningful exit hits, the math rebalances, and the donut fills in. And then, sooner than most professionals expect, a new donut opens at a higher altitude.

How the cycle plays out

The first time it shows up, the numbers are modest. You have $250,000 in liquid assets and a $1 million distribution is on the horizon. That distribution will feel transformative. This may be the first time you rethink your financial strategy. It may also reset your sense of what is possible, what is affordable, and what is appropriate to commit to the next fund. The donut fills in.

A few years later, you have $1 million in liquid assets and a $3 million distribution is on the horizon. The relative size of the gap is similar. Your lifestyle burn rate has increased. Your fund commitments have grown. You've gotten accustomed to a more elevated lifestyle. So has what you need your checking and brokerage balances to look like, because you now have a spouse and kids depending on it and you have gotten comfortable with the security a larger account balance provides.

The dollar amount that felt transformative in the first cycle now feels like the floor, not the ceiling.

What clients actually worry about

When professionals tell me they are worried about their financial situation, they are almost never talking about the next five or ten years. The long-term numbers are fine and they feel confident. They are talking about the next twelve to twenty-four months. The capital call schedule for the active funds. The deal that needs to close for the math to work. The uncertainty of a public market portfolio that can be impacted by tariffs, war, or AI-driven disruptions. The vacation home that came to market before you thought it would.

This is the built-in tension on the PE balance sheet that I find clients are least prepared for. The dollar value of the wealth is real. The accessibility of that wealth is constrained.

They have a solid income. They are comfortable with the investments inside the funds they help run. But juggling all of the inflows and outflows that sit outside the fund, the calls and deposits and tax bills and market noise, can feel overwhelming and uncertain in a way the long-term math never quite addresses.

Why this matters

In the donut hole years, the risk is concentration. For most professionals, PE is their single largest economic position by a wide margin, not to mention their income is tied to the asset class.

And when I think about private equity as an asset class, I think of it as long levered equity.

Whether you think about it that way or not, your funds likely move with the market and the broader economy.

To address this concentration, you can consider a more conservative posture with your liquid dollars. This is not about being defensive. It is about acknowledging what is already on your balance sheet. When markets are down, a liquid portfolio over-allocated to equities is what gets sold into the drawdown to meet calls or cover bills, often at the worst possible time. When markets are up, your career exposure is already capturing that growth, and at scale.

When you already have long levered equity exposure through your career, your liquid portfolio should not be doing the same job.

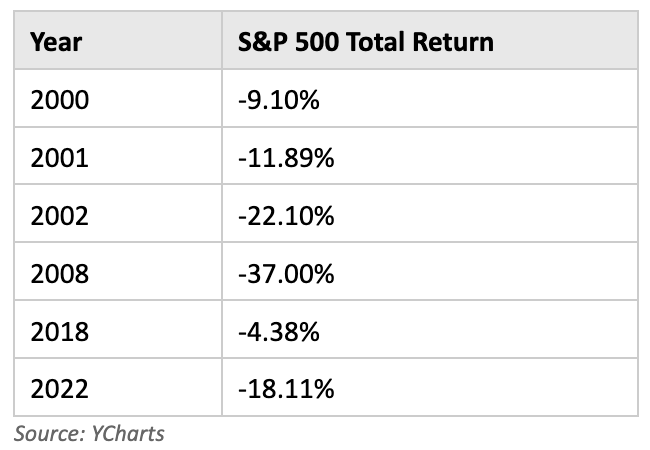

The S&P 500 makes the point quickly. From 2000 to 2025, the index posted a negative annual return six times:

The average return of those six down years is -17.1%. If any one of them lines up with a year your liquid balance sheet is supposed to do real work, whether that means meeting a capital call, paying a tax bill, or absorbing a soft stretch on the carry side, the math gets harder fast.

Planning for permanence

In my experience, how someone navigates the donut holes through their career has more to do with personality than circumstance. It tracks with overall risk tolerance, comfort level with carrying debt, and willingness to hold cash that is not pulling its weight on a return basis. Two clients with nearly identical balance sheets handle the same donut hole very differently because of how they are wired.

The clients who navigate it well plan for the gap as a permanent feature of the balance sheet, not a temporary problem to solve.

The donut fills in eventually. You will phase out of this dynamic at some point. It just tends to take longer than most professionals assume when they first enter the industry.

Plan for the hole, not the donut.

Important Disclosures:

Axiom Private Wealth, LLC ("Axiom") is a registered investment advisor. Advisory services are only offered to clients or prospective clients where Axiom and its representatives are properly licensed or exempt from licensure. The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor's particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor. The views expressed in this commentary are subject to change based on market and other conditions. These materials may contain certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur. Past performance shown is not indicative of future results, which could differ substantially. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. Asset Allocation may be used in an effort to manage risk and enhance returns. It does not, however, guarantee a profit or protect against loss. Diversification does not ensure a profit or guarantee against loss. All investments include a risk of loss that clients should be prepared to bear. The principal risks of Axiom's strategies are disclosed in the publicly available Form ADV Part 2A. Investing in foreign domiciled securities may involve risk of capital loss from unfavorable fluctuation in currency values, withholding taxes, from differences in generally accepted accounting principles or from economic or political instability in other nations. Investments in emerging or developing markets may be more volatile and less liquid than investing in developed markets and may involve exposure to economic structures that are generally less diverse and mature and to political systems which have less stability than those of more developed countries.

For additional information, please visit our website at www.axiomprivatewealth.com.

For current Axiom information, please visit the Investment Adviser Public Disclosure website at www.adviserinfo.sec.gov by searching with Axiom's full legal name or CRD #307388.